As a digital creator, I’ve witnessed the surging popularity of digital wallets, also known as e-wallets or mobile wallets. These innovative tools have revolutionized online payment methods, offering users a seamless and secure way to manage their financial transactions. Digital wallets enable individuals to store their payment information digitally, including credit card details and bank account information. In this article, we’ll delve into the workings of digital wallets, their myriad benefits, and the robust security measures in place to safeguard users’ sensitive data.

How Digital Wallets Work

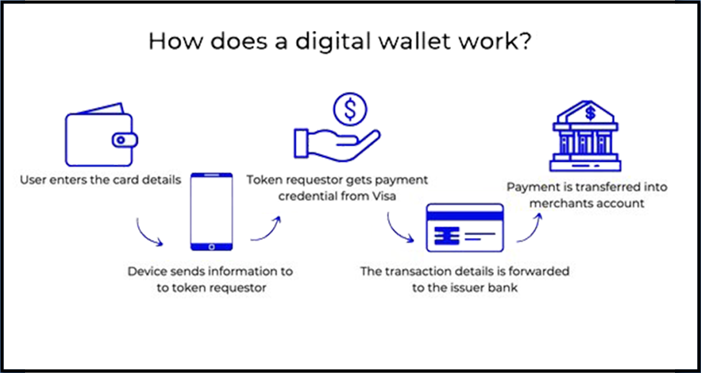

Digital wallets act as a bridge between consumers and merchants, facilitating seamless and secure transactions. Here’s a step-by-step breakdown of how digital wallets work:

- Account Creation: Users first need to create an account with a digital wallet provider. They are usually required to provide personal information and link their payment methods, such as credit cards or bank accounts, to the wallet.

- Adding Funds: After creating an account, users can top up their digital wallet by transferring funds from their bank account or credit card. Some wallets also allow users to receive funds from other users or merchants.

- Making Payments: When making a purchase, users can choose the digital wallet as their payment method. The wallet securely stores the payment information, eliminating the need to re-enter it for each transaction.

- Security Measures: Digital wallets employ various security measures to protect users’ sensitive information. These measures include encryption, tokenization, and two-factor authentication. Encryption ensures that data transmitted between the user’s device and the wallet’s servers is secure. Tokenization replaces sensitive payment information with a unique identifier, reducing the risk of data breaches. Two-factor authentication adds an extra layer of security by requiring users to verify their identity through a secondary method, such as a fingerprint or a one-time password.

- Transaction Processing: When a user initiates a payment, the digital wallet securely transmits the payment details to the merchant. The merchant’s payment gateway processes the transaction and sends a confirmation back to the digital wallet.

- Transaction Confirmation: Once the transaction is complete, the user receives a confirmation within the digital wallet app, providing details of the transaction, including the amount paid and the merchant’s information.

- Transaction History: Digital wallets maintain a transaction history, allowing users to review their past purchases and track their spending.

Benefits of Digital Wallets

Digital wallets offer several benefits to both consumers and merchants, including:

- Convenience: Digital wallets provide a convenient way to store payment information and make purchases with just a few taps on a smartphone or computer. Users no longer need to carry physical wallets or enter payment details repeatedly.

- Speed: Transactions made with digital wallets are typically faster than traditional payment methods. The payment information is already stored, reducing the time required to enter payment details for each transaction.

- Security: Digital wallets employ robust security measures to protect users’ payment information. Encryption, tokenization, and two-factor authentication help prevent unauthorized access and reduce the risk of fraud.

- Accessibility: Digital wallets are compatible with various devices, including smartphones, tablets, and computers. This allows users to make payments anytime and anywhere with an internet connection.

- Rewards and Loyalty Programs: Some digital wallets offer rewards and loyalty programs, allowing users to earn points or cashback on their purchases. These incentives can encourage users to adopt digital wallets and continue using them for their transactions.

- Contactless Payments: Many digital wallets support contactless payments, enabling users to make transactions by simply tapping their device on a compatible payment terminal. This feature is especially useful for in-store purchases, reducing the need for physical contact or the exchange of cash.

Security Measures in Digital Wallets

To ensure the security of users’ payment information, digital wallets implement various measures:

- Encryption: Digital wallets use encryption to protect data transmitted between the user’s device and the wallet’s servers. Encryption converts the payment information into a coded format, making it unreadable to unauthorized individuals.

- Tokenization: Tokenization replaces sensitive payment information, such as credit card numbers, with a unique identifier called a token. The token is used for transaction processing, while the actual payment details are securely stored on the wallet provider’s servers. This reduces the risk of exposing sensitive information in the event of a data breach.

- Biometric Authentication: Many digital wallets support biometric authentication, such as fingerprint or face recognition, to verify the user’s identity before allowing access to the wallet or authorizing a transaction. This adds an extra layer of security beyond traditional passwords.

- Two-Factor Authentication: Two-factor authentication requires users to provide an additional verification method, such as a one-time password sent via SMS or email, to access their digital wallet or complete a transaction. This helps prevent unauthorized access even if someone gains access to the user’s password.

- Fraud Monitoring: Digital wallets often employ sophisticated fraud monitoring systems to detect and prevent fraudulent transactions. These systems analyze transaction patterns, user behavior, and other factors to identify suspicious activity and trigger additional security measures if necessary.

- Device Security: Digital wallets rely on the security measures implemented by the user’s device, such as device encryption, screen lock, and operating system security updates. It is crucial for users to keep their devices secure by using strong passwords, enabling automatic updates, and installing reputable security software.

- Dispute Resolution: In the event of unauthorized transactions or disputes, digital wallets typically provide a resolution process to investigate and resolve issues. This may involve working with the user’s bank or credit card provider to reverse fraudulent charges and restore the user’s funds.

It is important for users to choose reputable digital wallet providers and regularly update their wallet app to ensure they have the latest security features and bug fixes.

Popular Digital Wallets

There are several popular digital wallet providers available, each offering unique features and compatibility with different devices and operating systems:

- Apple Pay: Apple Pay is a digital wallet available on Apple devices, including iPhones, iPads, and Apple Watches. It allows users to make secure payments both in-store and online using their Apple devices.

- Google Pay: Google Pay is a digital wallet available on Android devices. It enables users to make payments in-store, online, and within apps using their Android smartphones.

- Samsung Pay: Samsung Pay is a digital wallet available on Samsung devices. It supports contactless payments and can be used with both NFC-enabled payment terminals and traditional magnetic stripe card readers.

- PayPal: PayPal is a widely recognized digital wallet that allows users to make payments online and transfer money between individuals. It can be linked to bank accounts, credit cards, and debit cards.

- Venmo: Venmo is a digital wallet popular in the United States, known for its social payment features. It allows users to send and receive money from friends and family and make purchases at participating merchants.

- Alipay: Alipay is a digital wallet widely used in China. It offers a wide range of features, including payments, money transfers, bill payments, and access to various financial services.

- WeChat Pay: WeChat Pay is another popular digital wallet in China, integrated within the WeChat messaging app. It allows users to make payments, send money to friends, and access additional services within the WeChat ecosystem.

These are just a few examples, and there are many other digital wallet providers available worldwide, each with its own features and regional popularity.

Conclusion

Digital wallets have revolutionized the way we make payments, offering convenience, speed, and enhanced security. They provide a seamless and secure way to make purchases online and in-store, eliminating the need to carry physical wallets or repeatedly enter payment details. With robust security measures such as encryption, tokenization, and biometric authentication, digital wallets strive to protect users’ payment information and prevent unauthorized access. As digital wallets continue to evolve and gain popularity, it is important for users to stay vigilant, choose reputable providers, and follow best practices for securing their devices and personal information.

Be First to Comment